Foreclosure is overwhelming—even when you know it’s coming. Between missed payments, mounting legal notices, and the emotional strain of possibly losing your home, most people are just trying to survive the moment.

But in Texas, there’s another surprise many homeowners don’t expect:

You might still owe money even after your home is sold. The amount that remains unpaid after the foreclosure sale is considered your outstanding debt.

That’s because if the property sells for less than what you owe, your lender may try to collect the difference—called a deficiency—by filing a deficiency judgment in court.

If you’re facing foreclosure in Texas, this guide will help you understand what a deficiency judgment is

- How to avoid getting stuck with debt after foreclosure

- What a deficiency judgment is and how it works

- Texas-specific laws that affect whether you’ll owe money

What Is a Deficiency Judgment?

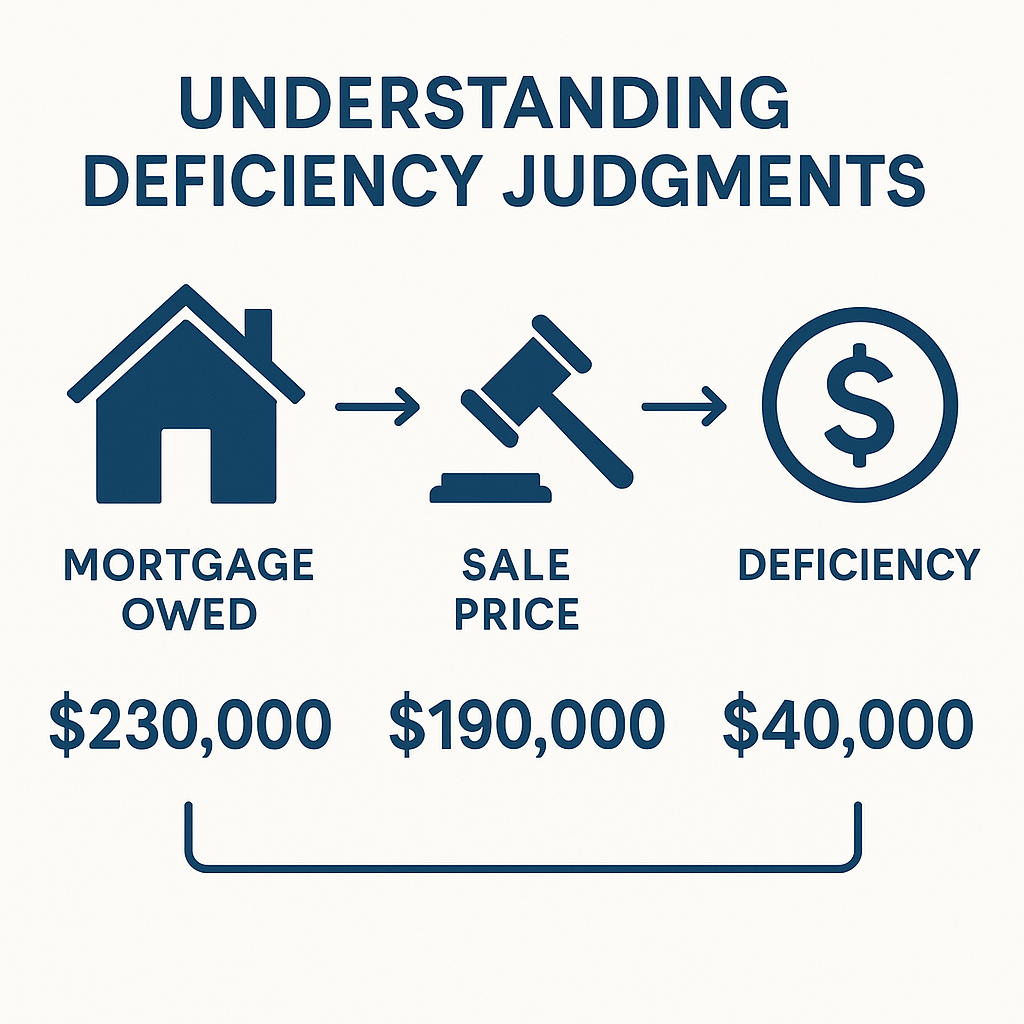

A deficiency judgment is a legal ruling that allows your lender to pursue you for the remaining balance on your loan after your home has been foreclosed and sold.

For Example:

- You owe $230,000 on your mortgage.

- Your home sells at foreclosure auction for $190,000.

- The $40,000 difference (unpaid balance) is called the deficiency.

- Your lender may file a lawsuit to recover that amount.

It’s important to understand:

✅ The foreclosure sale pays off part of your debt

❌ But it does not automatically erase everything you owe

After foreclosure, the borrower is the person liable for the deficiency owed—this is the specific amount the lender may seek to recover if the sale price is less than the secured debt.

If the lender wins a deficiency judgment in court, they can try to collect the balance through collection agencies, bank levies, or by placing liens on other assets you own.

And while many Texans think the foreclosure is “the end of it”—this separate legal action can reopen financial wounds for years if you’re not prepared.

Are Deficiency Judgments Allowed in Texas?

Yes, deficiency judgments are allowed in Texas, but they don’t happen automatically—and there are specific legal requirements lenders must follow to pursue one. Texas state law permits deficiency judgments in most cases following a foreclosure.

Texas foreclosure law falls under Section 51.003 of the Texas Property Code, which outlines what lenders must prove to collect a deficiency after a foreclosure sale. Texas has three different foreclosure processes: judicial, nonjudicial, and quasi-judicial.

Here’s what that means for you:

Texas Is a “Recourse” State (In Most Cases)

Unlike “non-recourse” states—where lenders can only take the property—Texas typically allows lenders to pursue the borrower personally for any remaining debt after foreclosure. Most foreclosures in Texas are nonjudicial, allowing lenders to foreclose without going to court if the loan contract contains a power of sale clause.

So, unless your mortgage was explicitly non-recourse (which is rare outside of specific investment loans), you’re likely on the hook for the balance unless the lender waives it in writing.

What the Lender Must Do to Pursue a Judgment

To collect a deficiency, your lender must:

- File an action brought in court after the foreclosure sale to recover the deficiency

- Prove the current fair market value of the property was less than what was owed on the mortgage

- Seek judgment only for the difference between the debt and the property’s fair market value—not just the auction price

Either party may make party requests or such a request to the court to determine the fair market value of the property during deficiency judgment proceedings.

🔎 Why this matters:

Texas law doesn’t automatically assume the auction price reflects the home’s true value. The court considers current fair market value, which can reduce or eliminate the deficiency claim. Texas law allows the borrower to get credit for the property’s fair market value when determining a deficiency judgment.

Example: How It Plays Out

Let’s say:

- You owed $250,000

- The property sold at auction for $200,000

- But the fair market value is determined to be $230,000

The lender can only pursue the difference between $250,000 and $230,000, which is $20,000—not the full $50,000 difference between your balance and the sale price. If the fair market value exceeds the foreclosure sale price, the court may apply an offset against the deficiency for the excess amount.

Important Notes

- Lenders only have 2 years from the foreclosure sale date to file for a deficiency judgment.

- If they miss the deadline, they lose the legal right to collect.

- Not all lenders pursue deficiency judgments—especially if the cost of litigation outweighs the expected recovery.

If you’re unsure whether your lender plans to pursue a judgment, it’s okay to ask them directly or check your foreclosure paperwork.

Related Articles

- Facing Foreclosure in Texas? Here’s What to Do

- Can You Owe Money After Foreclosure in Texas? Understanding Deficiency Judgments

- Foreclosure in Texas: How to Protect Your Credit and Sell Your Home

- Essential Resources for Avoiding Foreclosure and Stopping Foreclosure in Texas

- Understanding the Difference Between Judicial and Non-Judicial Foreclosure

- Key Differences: Which Is Better Foreclosure or Short Sale?

When Are You Most at Risk for a Deficiency Judgment?

Not all foreclosures result in a deficiency judgment. In fact, many lenders don’t pursue them—especially if they believe the borrower has no income or assets to collect from. Lenders will also assess the necessity of pursuing a deficiency judgment based on the likelihood of recovery.

That said, there are some situations where the risk of a deficiency judgment is much higher. Understanding these red flags can help you take steps to protect yourself in advance.

1. Your Home Sells for Much Less Than What You Owe

If your home sells well below your mortgage balance—whether due to market conditions or poor property condition—the lender has a bigger financial loss to recover, which increases the odds they’ll try to pursue it. The foreclosure sale results directly impact whether a deficiency judgment will be pursued, as lenders often look at the sale price compared to the outstanding loan balance to decide if they will seek to recover the difference.

This is especially common with homes needing major repairs, in declining neighborhoods, or where few buyers bid at auction.

2. You Have a Second Mortgage, HELOC, or Other Liens

Even if your primary mortgage lender chooses not to pursue a deficiency, junior liens—including second mortgages, HELOCs, and other subordinate claims—can still come after you personally for repayment.

These lienholders are often wiped out during foreclosure, meaning they don’t recover anything from the sale of the home. But that doesn’t mean the debt disappears. Deficiency judgments are not allowed for equity loans in Texas following foreclosure.

In Texas, each creditor holding a junior lien may still pursue you after foreclosure for the remaining balance.

💡 If you’re dealing with multiple liens on your property, you may find this helpful:

Selling a House with a Lien: A Homeowner’s Ultimate Guide

3. It Wasn’t Your Primary Residence

Lenders are generally more aggressive about pursuing deficiency judgments on investment properties, rental homes, or vacation houses.

Why? Because there’s no hardship protection or emotional argument—just numbers. You’re seen more like a commercial borrower.

4. You Didn’t Get a Deficiency Waiver in a Short Sale or Deed in Lieu

Many homeowners assume that if the lender approved a short sale or deed in lieu of foreclosure, they’re off the hook for the difference. But that’s only true if the lender provided a written waiver of deficiency.

If it’s not explicitly waived in the agreement, the lender may still pursue you—even if they helped you sell the home.

5. You Have Assets or Income Worth Pursuing

Even if you’ve fallen behind on your mortgage, lenders may assess the financial situation of borrowers when deciding whether to file a lawsuit.

If you:

- Own other real estate or vehicles

- Have a high-paying job or retirement savings

- Recently inherited money or sold a business

…you may be seen as collectible—even after foreclosure.

💡 TIP: How to Check If You Signed a Deficiency Waiver

If you completed a short sale or signed a deed in lieu of foreclosure, you may have agreed to terms that still leave you responsible for the remaining balance—unless the lender explicitly waived it in writing.

✅ Look for phrases like:

- “Borrower shall be released from any deficiency”

- “This agreement constitutes full satisfaction of the debt”

- “No further obligation shall remain after closing”

❌ Be cautious of vague language like:

- “Subject to investor approval”

- “This offer does not waive the lender’s right to pursue additional collection”

When in doubt, ask a real estate attorney or HUD-approved counselor to review your paperwork. A five-minute check could save you thousands.

How Do Lenders Collect After The Foreclosure Sale?

If a lender decides to pursue a deficiency judgment after foreclosure, it’s not automatic—they must actively file a lawsuit and prove the case in court. The lender will also consider the costs of litigation and collection when deciding whether to pursue a deficiency judgment. But if they succeed, the judgment becomes a legal debt you may be obligated to pay.

Here’s what that process looks like:

Step 1: The Lender Files a Lawsuit

Under Texas law, the lender has up to two years from the date of the foreclosure sale to file a deficiency claim.

- You’ll be served with legal papers and given a deadline to respond.

- If you don’t respond or show up to court, the lender may get a default judgment against you.

The deficiency claim may remain in a ‘pending determine’ status until the court rules on the fair market value and deficiency amount.

Step 2: The Court Determines Fair Market Value

Texas law protects homeowners from inflated collection claims by requiring the court to determine the property’s fair market value for the real property at the time the property is sold in foreclosure. The court’s determination is based on competent evidence, including expert opinion testimony, comparable sales, and other relevant data. Courts may also consider the future sales price, value applied to the future, holding costs, anticipated marketing time, marketing time, and cashflow generated when determining the property’s fair market value. While the sales price at which the property is sold is considered, the court may look at additional evidence to determine the fair market value. The value sought by the lender may be reduced by the court if the evidence supports a lower value. The court held, and courts have established, with clarification from the supreme court, that these standards apply in deficiency judgment cases.

- If the home sold for far less than market value, the court may reduce or deny the deficiency.

- You can present evidence like appraisals or CMA reports to support your case.

Step 3: If They Win, They Can Try to Collect

Once the judgment is issued, it becomes a collectible debt. The lender or a third-party debt collector may attempt to:

- Send collection notices or harassing calls

- Report the judgment on your credit

- Place liens on other property you own (like vehicles or land)

- Levy bank accounts or attempt garnishment (though Texas law restricts wage garnishment for consumer debt)

⚠️ Even if they never collect, the judgment can sit on your credit report and public record for up to 10 years, affecting future loan approvals and financial opportunities.

Can You Avoid a Deficiency Judgment?

The good news is: yes, you may be able to avoid a deficiency judgment altogether—but you have to be proactive.

Lenders don’t always pursue deficiencies, especially if they believe they won’t recover much or if you work with them early in the process. Here are the most common ways to avoid this type of post-foreclosure debt:

1. Sell the Home Before Foreclosure

If you act quickly enough, selling your home before the auction could allow you to pay off your mortgage (or at least negotiate with your lender). Even if the sale price is less than what you owe, you may be able to avoid a deficiency if:

- The lender agrees to a short sale and

- Provides a written deficiency waiver as part of the approval

💡 Cash buyers can often close quickly, helping you beat the auction deadline and avoid lasting credit damage or lawsuits.

2. Negotiate a Waiver in a Short Sale or Deed in Lieu

If you’re pursuing a short sale or signing a deed in lieu of foreclosure, make sure the agreement includes clear language waiving the lender’s right to pursue the deficiency.

- Ask for a “full satisfaction of debt” clause

- Don’t rely on verbal promises

- Get any waiver in writing and signed by the lender or their legal counsel

3. Work with an Attorney or Housing Counselor

Foreclosure laws are nuanced, and deficiency collections can get complex. An experienced attorney may be able to:

- Challenge the lender’s valuation of the property

- Negotiate a reduced payoff or settlement

- Get the case dismissed on procedural issues

If you can’t afford legal counsel, consider reaching out to a HUD-approved housing counselor—they can often help for free.

4. Consider Bankruptcy as a Last Resort

If a judgment has already been entered or is likely, filing Chapter 7 or Chapter 13 bankruptcy may allow you to:

- Discharge the debt entirely (Chapter 7)

- Or include it in a court-structured repayment plan (Chapter 13)

⚠️ Bankruptcy has long-term credit consequences, so it’s not a first option—but it may be worth exploring if your lender is actively pursuing collection.

What to Do If You’re Worried About a Deficiency Judgment

If you’re facing foreclosure—or you’ve already gone through it—it’s normal to feel anxious about whether you’ll owe more afterward. The uncertainty around deficiency judgments can be overwhelming, especially when legal and financial language feels confusing.

Here’s a step-by-step action plan to protect yourself and get clarity on what may happen next.

1. Ask for a Payoff and Reinstatement Quote

Before the foreclosure auction happens, request two figures from your lender:

- Payoff amount (the full amount needed to satisfy the loan)

- Reinstatement amount (just the amount needed to bring the loan current)

Knowing these numbers helps you:

- Understand your financial options

- Decide if a sale is possible

- Know what might still be owed

💡 These quotes are often only valid for a few days, so request updated versions if time passes.

2. Check Whether a Deficiency Judgment Is Likely

You can directly ask your lender (or their attorney) whether they plan to pursue a deficiency after foreclosure. While they may not commit to an answer, this can give you insight.

Also consider:

- Was the home your primary residence?

- Was a short sale or deed in lieu completed?

- Did you sign anything waiving the lender’s right to collect?

3. Document the Property’s Value

If a deficiency claim is filed, the court will consider your home’s fair market value—not just the auction sale price.

Start gathering:

- A recent appraisal (if available)

- A comparative market analysis (CMA) from a local agent

- Repair estimates (if condition lowered value)

Presenting competent evidence—such as expert testimony, comparable sales, and estimated holding costs—of the property’s value can help reduce or eliminate the deficiency.

4. Talk to a Housing Counselor or Attorney

If you’re unsure what your next step should be:

- Call a HUD-approved housing counselor

- Schedule a consultation with a foreclosure or bankruptcy attorney

💬 Many professionals offer free consultations, and housing counselors are often funded to help at no cost to you.

5. Take Action Early—Not After It’s Too Late

Once a judgment is filed, your options shrink. But before that happens, you may still be able to:

- Sell the home

- Settle with the lender

- Stop the foreclosure altogether

🏁 Final Thoughts: Don’t Let One Problem Turn Into Two

Going through foreclosure is already a difficult experience—but getting hit with a surprise deficiency judgment afterward can feel like pouring salt in the wound.

The key to avoiding that outcome? Act early, stay informed, and don’t assume it’s over when the house is sold.

Even if you’re underwater on the loan, you may still have time to:

- Sell your house before the auction

- Negotiate with the lender

- Avoid further legal or credit damage

💬 You are not powerless—there are still options.

Need Help Before the Auction?

If you’re facing foreclosure and worried about a potential deficiency judgment, TX Cash Home Buyers is here to help. We’ve worked with homeowners across Texas—including in Houston, Dallas, and Corpus Christi—to sell quickly and avoid further financial damage. Whether your auction date is weeks away or you just received notice, our local team understands the urgency and can walk you through your options—fast.

📞 Call (281) 595-7550 today! No pressure. Just real answers from a team that knows how to help

Frequently Asked Questions

What is a deficiency judgment in Texas?

A deficiency judgment in Texas is a court order that allows a lender to collect the remaining balance on a mortgage after a home is foreclosed and sold. If the property sells for less than what was owed, the lender may sue the borrower to recover the difference.

Can a lender sue me after foreclosure in Texas?

Yes, a lender can sue you after foreclosure in Texas if they believe you still owe money on the mortgage. This typically happens when the sale price of the foreclosed home is less than the remaining loan balance.

How long does a lender have to file a deficiency judgment in Texas?

A lender has up to two years from the date of the foreclosure sale to file a deficiency judgment in Texas. After that deadline, the lender loses the legal right to pursue the remaining balance.

Can you go to jail for not paying a deficiency judgment in Texas?

No, you cannot go to jail for not paying a deficiency judgment in Texas. Debt collection is a civil matter, not a criminal one. However, you may face lawsuits, collection actions, or asset liens if the judgment goes unpaid.

Does a deficiency judgment affect your credit?

Yes, a deficiency judgment can significantly affect your credit. If a lender wins a judgment against you, it may appear on your credit report for up to 10 years and lower your credit score by dozens of points.

Can I avoid a deficiency judgment by filing bankruptcy in Texas?

Yes, you may be able to avoid a deficiency judgment by filing bankruptcy in Texas. Chapter 7 can discharge the debt entirely, while Chapter 13 may allow you to repay it through a court-approved plan. Always consult a bankruptcy attorney before proceeding.

How can I avoid a deficiency judgment after foreclosure in Texas?

You can avoid a deficiency judgment in Texas by selling your home before foreclosure, negotiating a written waiver with your lender, or including the debt in a bankruptcy filing. Acting early gives you the best chance of avoiding legal action.

Disclaimer:

The content provided on this blog is for informational purposes only. We are not attorneys or tax professionals. For personalized legal or tax advice, please consult with a qualified professional.

Written by Lisa Martinez, Founder of TX Cash Home Buyers

About The Company

TX Cash Home Buyers helps Texas homeowners sell quickly and simply, even in tough situations like repairs, inherited homes, or financial stress. We’re known for our local experience, fair offers, and commitment to guiding sellers through off-market sales with clarity and care.